Updates

-

Review Your Insurance AnnuallyDecember 29, 2022

It is a good idea to periodically (at least annually) assess how your insurance

coverage compares to what you own or rent to and from others. A call to your

insurance agent can assist in determining if you have adequate coverage.

Be sure to mention what has changed since your policy was issued.Some changes are significant and can affect your coverage, so be

sure and discuss any changes you have made. Adding or removing wood heat, other

adults living in the home, renovations and purchases are examples of things you

should discuss with your agent. Please don’t wait for a claim to happen before

you contact your agent.Also consider an annual update to your personal inventory to be

sure you have a current list of all your belongings. If you don’t already have

a list, you can download a PDF file or order a hard copy

booklet for tracking your home inventory from the Missouri

Department of Insurance.This information is meant to be a broad overview and should not be the only source

you consult for evaluating your risk management needs. Adherence to the above

guidelines does not ensure coverage under your policy, nor does it guarantee

your risk will be accepted by our company or that your property or operations

are safe, healthful, or in compliance with laws, rules, or regulations.

Coverage is determined by specific policy provisions, limitations and

exclusions that can only be expressed in the policy itself. -

Navigating Roadways in WinterDecember 23, 2022

It’s officially winter, but Missouri has already experienced some winter weather. While the safest bet

during winter weather is to stay off the roads, some travel may be necessary.

If you must be on the road in such conditions, there are some things you can do

to prepare for potential hazards:· Allow for extra travel time.

· Travel at a safe speed and leave plenty of room between you and

other cars.· Clear all surfaces of your car before you embark on your journey.

· Be sure your cell phone is fully charged. Bring a charger along if you

have one that works in the car.· Tell someone where you are going and how long you expect it to take

you.· Make sure you have a full tank of gas in case you do become

stranded.· Do not leave your vehicle if you become stranded. Tie a bright

colored cloth to your antenna or door handle and attempt to contact

emergency personnel via cell phone if you have one.· If stranded, drivers should start and run their car for 10 minutes every

hour, using the heater. Be sure that your exhaust pipe and radiator

are clear of packed snow before running your engine. While the

engine is running, partially open a down-wind window to avoid carbon

monoxide poisoning and to get fresh air into the vehicle. Keep the

vehicle’s interior lights on while the engine is running. Avoid

hypothermia by constantly moving your arms and legs; clapping

hands will help keep you warm as well. Warning signs of hypothermia

are memory loss, disorientation, incoherence, slurred speech,

drowsiness, exhaustion, and uncontrollable shivering.This information is meant to be a broad overview and should not be the only source

you consult for evaluating your risk management needs. Adherence to the above

guidelines does not ensure coverage under your policy, nor does it guarantee

your risk will be accepted by our company or that your property or operations

are safe, healthful, or in compliance with laws, rules, or regulations.

Coverage is determined by specific policy provisions, limitations and

exclusions that can only be expressed in the policy itself. -

Check Your CreditDecember 19, 2022

As a consumer, you have a right to view your credit report from each of the three

credit reporting agencies (Experian, TransUnion and Equifax) each year. Visit annualcreditreport.com to

request the free report. You will have to pay to receive your credit score. It

is important to review your report to verify that the credit information

reported is accurate. Your credit report can affect your ability to finance

items like houses and cars, and it can even affect your potential employment or

your insurance rates. For more information on requesting the report, along with

instructions for what you can do if you find errors, visit the Federal Trade Commission website.If you have minor children, you can ask the credit bureaus if a

credit report exists for them. The Consumer Financial Protection Bureau (CFPB)

has an article with tips on how to do that. You can

request the file from any of the three bureaus. This is especially important if

you believe your child may have been the victim of identity theft. If you

discover that your child has a credit file, you can dispute the error. This tip sheet from the CFPB includes

information on how to dispute the credit file for your child.This information is meant to be a broad overview and should not be the only source

you consult for evaluating your risk management needs. Adherence to the above

guidelines does not ensure coverage under your policy, nor does it guarantee

your risk will be accepted by our company or that your property or operations

are safe, healthful, or in compliance with laws, rules, or regulations.

Coverage is determined by specific policy provisions, limitations and

exclusions that can only be expressed in the policy itself. -

Identity Thieves Hone in on Busy Shoppers and TravelersDecember 14, 2022

While you’re making plans for the holidays with family and friends, cyber criminals are looking for

opportunities to steal your identity and commit financial frauds. Between 2014

and 2018, there was a 109% increase in holiday identity fraud. There are

five ways individuals experience greater risk of identity theft around the

holidays:1. You’re distracted. As you rush around to stores and holiday parties,

you’re more likely to forget your purse, lose your wallet or have

a credit card stolen. When you’re distracted, you are less likely to spot

a phishing email before it’s too late.2. You use public WiFi or charging stations. Public WiFi networks are

not secured by a password, and when you use your device on an

open network, your data is at risk of being stolen. The best rule is

never to use public WiFi and especially not for financial transactions

and shopping. A newer vulnerability exists at public charging stations.

Data thieves hack into these stations and “juice jack” unsuspecting

victims’ devices by pulling data through the USB cords on phones.3. You are bargain hunting online. Research shows that 43% of holiday

shopping identity theft occurs online. One minute you’re Googling

frantically for hard-to-find holiday gifts and the next minute, you’ve

suddenly found them in stock and unbelievably priced for a fire sale.

Watch out! This is how bargain hunters get suckered into fake web

stores. They steal your card number and identity…and you don’t even

get the items you bought.4. Your credit card gets “skimmed.” Sometimes thieves insert a credit

card skimmer inside the card machines in gas stations, retail stores

or restaurants. Unbeknownst to the store, every customer’s credit

card information is being swiped by cybercriminals.5. You fall for a holiday charity scam. You’re feeling extra generous

during the holiday season and you give generously when asked for

charitable donations. Unfortunately, some criminals use fake charities

to tug on your holiday heartstrings. Do your homework before donating. -

Security Tips for the Holiday SeasonDecember 06, 2022

Just a few friendly reminders on how you can take steps to help protect your home from burglars and

other potential harm if you plan to be away from home this holiday season.

Portions of this were taken from an article on www.safewise.com.1. If you can afford a home security system or security cameras of any kind,

those are both great ways to protect your home. If you can’t afford those,

you can try putting a security sign in your yard or setting up a dummy camera

to convince would-be burglars that you do have one.2. Don’t advertise your travel plans on social media.

That just gives burglars a precise schedule to

find your home unoccupied. Post those pics after you return home.3. Install motion sensors on any outdoor lights you have. Use a timer

on Christmas lights to make sure they come on as scheduled while

you are gone.4. Consider leaving on a radio or TV during the day that could convince

a burglar that someone is in the home.5. This seems pretty obvious, but lock your doors and windows. This

includes keeping your garage door closed as much as possible.

An open garage door may seem like an invitation, and it

shows off your stuff to passersby.6. If you are going to be away for more than a couple of days,

have the Post Office hold your mail and stop any newspaper deliveries.

You could also ask a friend or trusted neighbor to pick up your mail and papers.

Nothing signals an absence like a pile of newspapers in the driveway.7. Be friendly to your neighbors. Having a good relationship with those

who live around you can supply an additional layer of security for your

home. They can keep an eye out when you are gone, and you can

return the favor when they leave home.8. Reduce the landscaping around your home.

This may seem like an odd addition to the list, but bushes

and shrubs around a home make good hiding spots.9. At Christmastime, keep packages out of view of the windows.

Passersby shouldn’t be able to tell how many packages little Suzie

has under the tree.10. Consider contacting your local police department to do a check of

your house. They might be able to suggest things you could do to

improve security.This information is meant to be a broad overview and should not be the only source

you consult for evaluating your risk management needs. Adherence to the above

guidelines does not ensure coverage under your policy, nor does it guarantee

your risk will be accepted by our company or that your property or operations

are safe, healthful, or in compliance with laws, rules, or regulations.

Coverage is determined by specific policy provisions, limitations and

exclusions that can only be expressed in the policy itself. -

All is Calm, All is BrightNovember 29, 2022

Hanging outdoor lights is a popular tradition, and many people enjoy taking their

decorating game to the next level, and still more like seeing elaborately

decorated homes and businesses. Whether you are an avid, experienced

light-hanger or a first-timer, there are lots of things to consider and some

safety to keep in mind. This post from Lowe’s offers some basic tips for

anyone wishing to light up their home this Christmas. Make sure you have the

right tools and be safe out there displaying your holiday spirit!This information is meant to be a broad overview and should not be the only source you consult for evaluating

your risk management needs. Adherence to the above guidelines does not ensure

coverage under your policy, nor does it guarantee your risk will be accepted by

our company or that your property or operations are safe, healthful, or in

compliance with laws, rules, or regulations. Coverage is determined by specific

policy provisions, limitations and exclusions that can only be expressed in the

policy itself. -

Tips to Avoid Familiar FraudNovember 21, 2022

This post comes from CyberScout, one of Barton Mutual’s partners in providing cyber liability

insurance to our policyholders. If you are interested in cyber insurance for

yourself or your small business, contact one of our independent agents today.1. Use strong passwords and password protect computers and mobile devices. If you have trouble keeping

track of passwords, consider a password generation and storage tool.2. Always keep passwords and PIN numbers private—even from friends and family.

3. Share minimal personal information on social media.

4. Set social media privacy options to conservative levels.

5. If you have young children, ask the credit bureaus whether a credit file exists for your child.

If yes, place a credit freeze on the file and start to remediate any fraud.6. List a fake birthday on nonofficial sites such as social media. Pick one you can easily remember that is

close to your birthday, but a little different.7. Obtain a credit and identity monitoring service to stay vigilant against familiar fraud and other

financial identity theft. -

Military Family AppreciationNovember 15, 2022

The month of November has been proclaimed a

month to celebrate veterans and military families. We are extremely grateful to

all the men and women who serve this great nation in our military branches. We

also know that those brave souls depend on their families for love and support

while at home and serving abroad. To enlist in the military is to accept that

personal sacrifice must be made, and the family members who stand beside those

servicemen and women have sacrifices to make as well. To all who serve and who

have served and to those who love those service members, you have our eternal

gratitude. -

Safe Online Shopping GuidanceNovember 08, 2022

Smartphones and the Internet have revolutionized the way consumers shop. Armed with a few search

terms and simple clicks, we can find items, compare prices, read product

reviews, order, and pay for all types of items from electronics, appliances,

and tools to furniture, clothes, and groceries. Often, consumers also have the

power to choose whether purchases will be picked up in store or delivered right

to our doorstep. Any way you look at it, online shopping is a fast and

convenient way to buy what we want and need.Online convenience also comes with some risk. Sometimes consumers don’t receive exactly what they

ordered; get scammed by fraudulent websites; or become victims of identity

theft and/or loss. Cybercriminals are opportunistic, and they will be seeking

to exploit the growth in online shopping this holiday season. But don’t worry,

with a little preparation and vigilance, consumers can safely and securely shop

online and avoid falling victim to scams.Since cybercrime is largely motivated by money, that makes Black Friday and Cyber Monday very

attractive targets for cybercriminals. And that means increased phishing

attempts that try to get you to reveal personal information, account

credentials, and credit card numbers. Through email, fake ads, and illegitimate

websites, cybercriminals are hoping some unwitting consumers will let their

guard down in the rush to secure the best deals before they’re gone.Since consumers often spend more than usual during the holiday season, it’s easy to lose focus when

an email or text message arrives under the guise of your credit card provider

or bank regarding a suspicious transaction or frozen account. Without prior

awareness of these scams, some consumers mistakenly click on links or share

their personal information. Instead, consumers should be aware of these and

other common attacks and use caution to avoid falling victim.Knowledge is power. Enjoy your online shopping experience by following best practices and increase

your awareness of common scams. These eight tips can help you get the deals and

avoid the scams:1. Use familiar websites and know thy vendors.

Before providing any personal or financial information, be sure

that you are doing business with a reputable, established vendor. Verify the

legitimacy of the website by reviewing certificate information, including who

it was issued to. Check the BBB’s online directory and scam tracker or search

retailer reviews on Google.2. Look for the ‘s’ and the lock.

Always look for the security symbol, such as an unbroken padlock in the address

bar and URLs that start with ‘https’. This ensures that your information is

protected with encryption.3. Avoid phishing and social engineering attacks.

Be wary of unsolicited email requesting information from you,

such as fake invoices or shipping notifications. Legitimate businesses don’t

ask for information via email. Instead of responding to the email or clicking

on links, type in the merchant’s authentic website address yourself and log in

to check your account.4. Be aware of common tricks.

Educate yourself about common online scams to avoid falling for

too-good-to-be-true deals, including rock-bottom prices form unknown internet

retailers, fake ads and social media offers, gift card scams, and more.5. Use credit, not debit.

Credit cards offer an extra level of protection from fraudulent charges that may not be available

with a debit card. You can add additional purchase protections by using a

payment gateway like PayPal, Good Wallet, or Apple Pay. Secure payment gateways

stop purchase data from being intercepted by hackers.6. Monitor your statements and verify receipts.

Keep records of your purchases, including confirmation pages or

email receipts, to compare with your bills and statements. If there is a

discrepancy, report it immediately.7. Always use strong passwords.

Simple and commonly used passwords allow hackers to easily gain access and control of your online

accounts, change shipping addresses, and make purchases using your credit

cards.8. Don’t purchase over public Wi-Fi.

If you shop using your mobile phone, stay on your carrier’s cellular network.

Free public Wi-Fi can be much less secure.CyberScout®—We’ll take it from here.™

CyberScout is leading the charge against hackers and thieves, providing identity management, credit

monitoring and cyber security for more than 17.5 million households and 770,000

businesses. Contact your bank, credit union, insurance company or employer to

find out if they offer CyberScout services.This information is meant to be a broad overview and should not be the only source

you consult for evaluating your risk management needs. Adherence to the above

guidelines does not ensure coverage under your policy, nor does it guarantee

your risk will be accepted by our company or that your property or operations

are safe, healthful, or in compliance with laws, rules, or regulations.

Coverage is determined by specific policy provisions, limitations and

exclusions that can only be expressed in the policy itself. -

Winter is ComingNovember 04, 2022

Like it or not, colder weather is bearing down on Missouri. As we press on toward winter, make sure

your property is prepared and your insurance policy is equipped to provide

coverage in the event of a winter weather loss.· Always maintain heat during winter months, even in vacant dwellings/businesses. If you are going to be away

from your home, you can reduce the heat so it won’t run as much, but ensure

it’s not too low, as water lines in exterior walls could freeze in times of

extreme wind chill or temperature drops.· Winterize your pipes when possible and, again, maintain heat at an appropriate level; simply leaving

it above freezing will most likely not be sufficient. Freezing pipes and the

resulting damage may not be a covered loss under certain types of insurance

policies. In addition, policies that do contain coverage for the peril of

freezing may not cover loss that results from your failure to maintain heat or

properly winterize the structure.· Turn off the water and winterize the lines at your home if you’re leaving for a few days. This can

mitigate the possibility of a water-related loss while you are away.Check with your insurance company or agent if you need help understanding your policy, and

brace yourself for winter!This information is meant to be a broad overview and should not be the only source you consult

for evaluating insurance coverage or purchase. The description of coverages and

programs are purposely brief and are subject to specific policy provisions,

limitations and exclusions that can only be expressed in the policy itself. For

a complete explanation of coverages, please consult one of our licensed agents. -

National Cyber Security MonthOctober 25, 2022

Every day, we place our private data in the hands of other companies and individuals and trust them to keep it safe. Every day, bad actors are trying to steal that data. Unfortunately, some of them succeed.

T-Mobile recently announced a data breach affecting 7.8 million customers. They estimate an additional 40 million records were stolen from past or prospective customers.

While no one can guarantee you protection from such a breach, you can take steps to insulate yourself from the aftermath of a stolen identity or other cybercrimes. Barton Mutual has partnered with Berkley Re to offer cyber liability coverage on many of our policies.

For our commercial policies, the coverage is optional and will offer assistance with a breach:

The Standard Aggregate inclusive of all coverages above is $25,000, with optional limits available of $50,000, $100,000 and $250,000. These coverages include additional services, such as:

For most owner-occupied personal lines policies, the coverage is included and provides the following benefits:

Services for personal lines coverage include:- First-Party Privacy Breach Expense, including up to $10,000 each for Extortion Threat Expenses, and Data Replacement and System Restoration Expense

- Third-Party Cyber Liability Coverage, including up to $10,000 for PCI Fines

- Regulatory Proceeding Claim Expense, including up to $10,000 for Regulatory Fines

- Optional First-Party Business Interruption, which equals 25% of the aggregate limit.

- Notification letter preparation, printing and mailing

- Toll free number to Sontiq’s Resolution Center

- Call handling

- Credit monitoring and fraud alerts

- Fraud resolution services

- Investigative and forensic services

- Online Extortion. Expenses and ransom paid for threats to cause a network disruption.

- Cyber Bullying Response. Costs for counseling, tutoring, temporary relocation, tuition expense.

- Identity Theft. Costs and help in reclaiming your policyholder’s identity.

- System Compromise. Data recovery and system restoration needs.

- Internet Clean Up. Expenses associated with removing false statements on the internet.

- Breach Cost. Costs associated with notification, investigation and monitoring a breach.

- Social Engineering. Costs that arise from the intentional misleading of an individual which leads to the insured willingly sending money to a fraudster.

Identity Management

Ransomware

Breach Protection

Educational Services

Sontiq Claims

This information is meant to be a broad overview and should not be the only source you consult for evaluating your risk management needs. Adherence to the above guidelines does not ensure coverage under your policy, nor does it guarantee your risk will be accepted by our company or that your property or operations are safe, healthful, or in compliance with laws, rules, or regulations. Coverage is determined by specific policy provisions, limitations and exclusions that can only be expressed in the policy itself.- Provides unlimited 24/7 service and support to help minimize damage and resolve identity theft incidents.

- Diagnose the issue and implement a plan to protect data.

- Get access to highly experienced professionals with deep expertise in information security, data privacy and governance.

- Receive customized ransomware risk assessment and prevention services.

- Investigation of a breach and corresponding legal requirements.

- Notification services to alert anyone affected by a breach.

- Monitoring provided for those affected by a breach.

- Partnership with Nobully.org, a nonprofit working to eradicate cyberbullying worldwide.

- Alerts on the latest scams, fraud attempts and ways to prepare.

- Alerts on the latest malware and how to stay safe online.

- Personalized handling of any cyber liability claim.

-

Get Smart About CreditOctober 20, 2022

As a consumer, you have a right to view your credit report from each of the three

credit reporting agencies (Experian, TransUnion and Equifax) each year. Visit annualcreditreport.com to

request the free report. You will have to pay to receive your credit score. It

is important to review your report to verify that the credit information

reported is accurate. Your credit report can affect your ability to finance

items like houses and cars, and it can even affect your potential employment or

your insurance rates. For more information on requesting the report, along with

instructions for what you can do if you find errors, visit the Federal Trade Commission website.If you have minor children, you can ask the credit bureaus if a

credit report exists for them. The Consumer Financial Protection Bureau (CFPB) has

an article with tips on how to do that. You can

request the file from any of the three bureaus. This is especially important if

you believe your child may have been the victim of identity theft. If you

discover that your child has a credit file, you can dispute the error. This tip sheet from the CFPB includes

information on how to dispute the credit file for your child.This information is meant to be a broad overview and should not be the only source

you consult for evaluating your risk management needs. Adherence to the above

guidelines does not ensure coverage under your policy, nor does it guarantee

your risk will be accepted by our company or that your property or operations

are safe, healthful, or in compliance with laws, rules, or regulations.

Coverage is determined by specific policy provisions, limitations and

exclusions that can only be expressed in the policy itself. -

World Mental Health DayOctober 10, 2022

According to the National Alliance on Mental Illness, one in

five US adults struggles with a mental illness. This life brings us much joy,

but it also brings high stress levels, mood swings, and bad eating habits. The

best way to beat that mindset is to take care of yourself, disclose the situation

to others, and get additional support. For more tips on what steps are next please

visit http://www.bcmhsus.ca/about/news-stories/stories/10-tips-to-boost-your-mental-health

or https://www.nami.org/Your-Journey/Individuals-with-Mental-Illness. -

Financial Planning MonthOctober 03, 2022

Adequate insurance coverage is animportant part of any financial plan. Some common areas that may be overlooked

include home-based business coverage, equipment breakdown coverage, insured

values on property (especially if improvements have been made), and ACV vs.

replacement cost coverage. It might also be a good idea to review the

deductible on your policies to be sure you are financially capable of assuming

that cost in case of a covered loss. Your insurance agent can help you

understand your coverages and determine if you are adequately covered in case of a loss.Please reach out to us if you need help understanding any of the coverages on any

policy you have written with us. You can reach our office at 417-843-6265

Monday-Friday 8:00 AM – 4:30 PM Central. You can also email

our Customer Service department any time.This information is meant to be a broad overview and should not be the only source

you consult for evaluating your risk management needs. Adherence to the above

guidelines does not ensure coverage under your policy, nor does it guarantee

your risk will be accepted by our company or that your property or operations

are safe, healthful, or in compliance with laws, rules, or regulations.

Coverage is determined by specific policy provisions, limitations and

exclusions that can only be expressed in the policy itself. -

Why did the Limit on my Dwelling/Building Increase?August 16, 2022

Barton Mutual employs an automatic increase feature in most of our policies. Sometimes known as inflation guard, this feature increases your dwelling/building coverage when the policy renews to help keep up with inflation and the rising costs of building materials and construction. Though we increase your dwelling/building coverage annually, this is no guarantee your dwelling/building is adequately insured. It is the responsibility of the policyholder to determine adequate coverage. Contact your agent if you need help determining the adequate coverage amount for your property. It is also important that you notify your agent if you make significant changes that increase the value of your property.

This information is meant to be a broad overview and should not be the only source you consult for evaluating insurance coverage or purchase. The description of coverages and programs are purposely brief and are subject to specific policy provisions, limitations and exclusions that can only be expressed in the policy itself. For a complete explanation of coverages, please consult one of our licensed agents.

-

Fun on the Water!May 31, 2022

This weekend will signal the start of summer for many folks. Lakes across the state will welcome visitors for water recreation. Don’t find yourself in hot “water”—make sure you are adequately covered for this exposure. Property coverage for your boat and related equipment can be added to most of our personal lines policies. Also, liability coverage is available to protect you in the event a covered lawsuit is filed against you resulting from the use of your watercraft. Contact one of our local agents for a quote today. -

Risky DataMay 03, 2022

When our lives move quickly, we sometimes risk data security in exchange for convenience or instant gratification. However, seemingly small decisions result in deep and lasting consequences if you lose your identity. Here are a few common scenarios that pose outsized risk to your security:

- You receive an offer in the mail that you don’t want—so you just throw it in the trash, not realizing that there’s a lot of information about you inside.

- You’re having fun on vacation but remember your electric bill is due, so you log into online banking using public WiFi at the nearest coffee shop.

- An online store requires you to set up an account and provide additional data prior to your purchase—but the website is “http” (or unsecured). When you set up the account, you used the same password you always do—Fifi12345 after your beloved dog.

- After getting cash, you drove away and left your receipt hanging in the ATM.

- Your friends all played a question game on Facebook, so you played too. Your answers revealed personal information that could help a hacker answer your “forgot my password” questions, such as your pet’s name, your first car, etc.

These are common mistakes people make every day. More than one in four Americans don’t shred their mail, leaving personal information intact for dumpster-diving fraudsters. 1 A recent Experian study revealed that 70 percent of consumers globally are “willing to share more personal data” with online organizations, especially if they believe it will provide greater security or convenience. 2 Two in three adults admit to reusing passwords. 3

We have partnered with Sontiq to offer comprehensive identity management services.

1 “Poll: Americans Leave Their Personal Information Open to Thieves,” Creditcards.com, February 2019

2 2019 Global Identity and Fraud Report, Experian

3 “Google Survey Finds Two in Three Users Reuse Passwords,” Info Security Magazine, February 2019

This information is meant to be a broad overview and should not be the only source you consult for evaluating your risk management needs. Adherence to the above guidelines does not ensure coverage under your policy, nor does it guarantee your risk will be accepted by our company or that your property or operations are safe, healthful, or in compliance with laws, rules, or regulations. Coverage is determined by specific policy provisions, limitations and exclusions that can only be expressed in the policy itself.

-

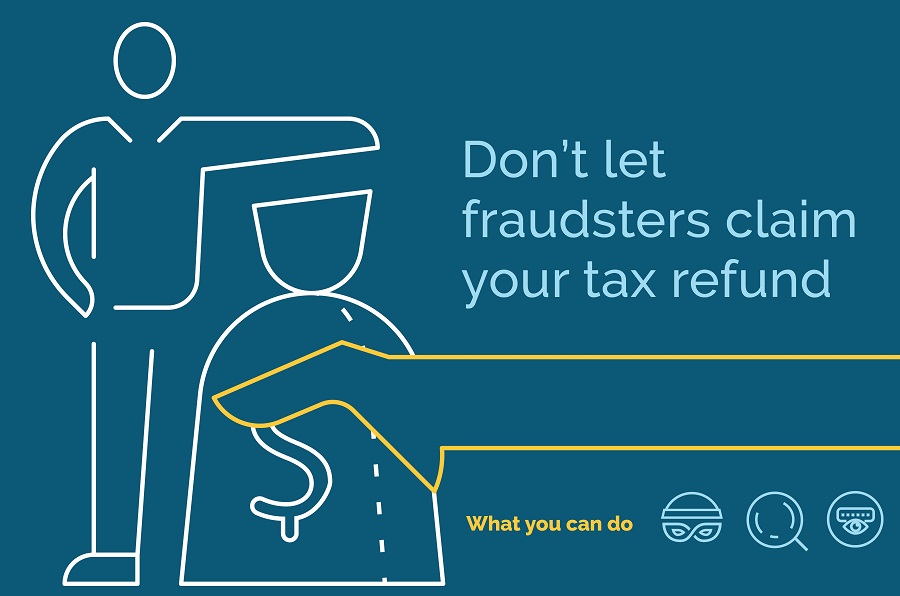

Protect Your Tax Return From Identity ThievesApril 04, 2022

Over the past several years, the IRS actions against tax identity fraud were successful in driving down the rate of tax fraud. Then the COVID-19 pandemic happened. The IRS extended due dates and become bogged down trying to process returns while keeping their employees safe. Additionally, U.S. stimulus payments were administered as tax refunds and the Federal government enhanced state unemployment benefits. Identity thieves had more financial incentive than ever before to commit tax and benefits fraud.The impact was immediate: By the end of February 2020, tax return identity theft was already up 751% year over year.1 By June, 892,777 tax returns had been flagged by the IRS for potential identity theft.2 But there’s good news—you can take steps now to protect your identity as well as any tax refunds or stimulus payments due to you in 2022.

How tax return fraud happens

Tax-related identity theft can leave taxpayers bewildered and frustrated, but the mechanics of it are fairly simple. First, identity thieves obtain sensitive information about you including your name, address, and personal tax identification number. They can either buy the information from criminal sources or trick you into giving it to them through phishing or phone scams. Then they use it to file a tax return using a false address or post office box and wait for the refund check to roll in.

Warning signs of tax return fraud

There are several warning signs that indicate you may be a victim of tax return fraud:

- The IRS or other taxing authority rejects your attempt to file your tax return.

- The taxing authority requests verification of your identity, indicating something may be amiss.

- Income is reported by two or more employers, most likely because someone else has used your tax identification number to gain employment. Your return could be flagged for failing to pay sufficient taxes on wages or to report all wages.3

Take advantage of the new IRS Identity Protection PIN

In January, the IRS expanded the Identity Protection PIN Opt-In Program to all taxpayers who can verify their identities.4 The Identity Protection PIN (IP PIN) is a six-digit code you establish with the IRS that is only known by the agency and you. The IP PIN provides a good way to lock out identity thieves and prevent them from filing fraudulent tax returns using your personal information. The IP PIN is valid for one calendar year, so mark your calendar to obtain a new one at the start of each year.

Resolve tax-related identity theft

If you discover you have become a victim, follow these steps:

- Contact your taxing authority and fill out identity theft paperwork.

- File your correct return using the instructions they provide you.

- Contact the credit bureaus and place a fraud alert on your account.

- Respond promptly to all correspondence from your taxing authority.

- Keep excellent records of all of your correspondence and filings.

- Add a credit monitoring and identity protection service to identify any further identity theft or fraud in other areas of your life.

We have partnered with Sontiq to offer comprehensive identity management services. Contact a local independent agent today to see how you can get a policy containing cyber protection with Barton Mutual.

1 “Interim Results of the 2020 Filing Season,” Treasury Inspector General for Tax Administration, April 7, 2020.

2 “Interim Results of the 2020 Filing Season: Effect of COVID-19 Shutdown on Tax Processing and Customer Service Operations and Assessment of Efforts to Implement Legislative Provisions,” Treasury Inspector General for Tax Administration, June 30, 2020.

3 “Taxpayer Guide to Identity Theft,” IRS website, page updated October 22, 2019.

4 “All taxpayers now eligible for Identity Protection PINs,” IRS, January 12, 2021.

-

Groundhogs as MeterologistsJanuary 24, 2022

Have you ever wondered why we have Groundhog Day and how February 2 was chosen? According to an article on History.com, the “holiday” was first celebrated on February 2, 1887. That day falls about midway between the winter solstice and spring equinox. The groundhog made famous at that event, Punxsutawney Phil, only has about a 50% success rate in predicting the severity of our remaining winter. Another famous rodent, Staten Island Chuck, actually boasts an 80% success rate.One thing we know for sure: the spring equinox comes on March 20. From now until then (and beyond), we can count on the weather in Missouri being unpredictable no matter what the groundhog says!

-

Berkley Re Solutions and Barton Mutual to Bring a New Workplace Violence Program Solution to MarketNovember 04, 2021

Liberal, MO — Berkley Re Solutions and Barton Mutual announce the creation of a new Workplace Violence Protection insurance program available January 1, 2022 to all of Barton’s existing commercial customers and new business, as an endorsement to Barton’s commercial lines policies.

“Unfortunately, workplace violence is a reality. Businesses, both large and small, located in the city or in rural areas, are too often faced with these devastating events. The insurance industry has long been trusted to help businesses in their greatest times of need. Bringing this combined insurance and services solution quickly to our customers and agents continues our solemn responsibility and commitment,” said Brian King, President/CEO, Barton Mutual.

Greg Douglas, President, Berkley Re Solutions said, “We developed this new, reinsured, turn-key program with guidance and input from multiple commercial insurance carriers across the U.S. We’re delighted that Brian, his leadership team, and their Board decided to move swiftly to have Barton Mutual partner with us as the first commercial insurance carrier in Missouri, and the United States, to offer this important program. Barton’s commitment to their agents and insureds has been abundantly clear as we’ve worked to quickly implement this Workplace Violence product.”

The Workplace Violence insurance program offers 10 unique coverages/services, including crisis management, business income, mental health counseling, public relations expense, security services, and more. With a broad coverage cause of loss, coverage also includes an off-premises extension that follows insureds where they go while conducting their business. And while indemnification is important, the crisis management services are critical to the overall solution and are included automatically. What insureds desperately need in these devastating times are experts who know how to guide insureds through these complicated events.

About Barton Mutual:

Barton Mutual has provided property and casualty coverage since 1894, extending throughout the state of Missouri from Main Street in Liberal. More than 450 agency locations in the state function as points of sale for Barton Mutual Insurance. Barton Mutual Insurance Company has been assigned a Financial Stability Rating® of A, Exceptional, from Demotech, Inc. For more information about Demotech or FSRs, visit www.demotech.com or call (800) 354-7207. For more information about Barton Mutual, please visit https://bartonmutualgroup.com/.

About Berkley Re Solutions:

Berkley Re Solutions, a Berkley Company®, is the innovative choice to provide collaborative product development, insurance and reinsurance solutions for you and your multiple stakeholders. We are dedicated casualty reinsurance specialists and provide exceptional financial security and utilize global knowledge and expertise to offer you thoughtful solutions. We operate locally and focus on producing industry leading returns with and for our clients. For more information, please visit https://www.berkleyre.com/solutions/custom-turnkey-solutions/workplace-violence-coverage/.

Reinsurance products and services may be provided by one or more insurance company subsidiaries of W. R. Berkley Corporation. Not all such products and services are available in every jurisdiction, and the precise coverage afforded by any insurer is subject to the actual terms and conditions of the policies as issued. Berkley Re Solutions is a member company of W. R. Berkley Corporation, whose insurance company subsidiaries are rated A+ (Superior) by A.M. Best Company.

-

October is Financial Planning MonthOctober 22, 2021

Adequate insurance coverage is an important part of any financial plan. Some common areas that may be overlooked include home-based business coverage, equipment breakdown coverage, insured values on property (especially if improvements have been made), and ACV vs. replacement cost coverage. It might also be a good idea to review the deductible on your policies to be sure you are financially capable of assuming that cost in case of a covered loss. Your insurance agent can help you understand your coverages and determine if you are adequately covered in case of a loss.Please reach out to us if you need help understanding any of the coverages on any policy you have written with us. You can reach our office at 417-843-6265 Monday-Friday 8:00 AM – 4:30 PM Central. You can also email our Customer Service department any time.

This information is meant to be a broad overview and should not be the only source you consult for evaluating your risk management needs. Adherence to the above guidelines does not ensure coverage under your policy, nor does it guarantee your risk will be accepted by our company or that your property or operations are safe, healthful, or in compliance with laws, rules, or regulations. Coverage is determined by specific policy provisions, limitations and exclusions that can only be expressed in the policy itself.

-

Prepare for WinterOctober 19, 2021

Like it or not, winter is just around the corner. As temperatures drop in the coming weeks, make sure your property is prepared and your insurance policy is equipped to provide coverage in the event of a winter weather loss.

- Always maintain heat during winter months, even in vacant dwellings/businesses. If you are going to be away from your home, you can reduce the heat so it won’t run as much, but ensure it’s not too low, as water lines in exterior walls could freeze in times of extreme wind chill or temperature drops.

- Winterize your pipes when possible and, again, maintain heat at an appropriate level; simply leaving it above freezing will most likely not be sufficient. Freezing pipes and the resulting damage may not be a covered loss under certain types of insurance policies. In addition, policies that do contain coverage for the peril of freezing may not cover loss that results from your failure to maintain heat or properly winterize the structure.

- Turn off the water and winterize the lines at your home if you’re leaving for a few days. This can mitigate the possibility of a water-related loss while you are away.

Check with your insurance company or agent if you need help understanding your policy, and brace yourself for winter!

This information is meant to be a broad overview and should not be the only source you consult for evaluating insurance coverage or purchase. The description of coverages and programs are purposely brief and are subject to specific policy provisions, limitations and exclusions that can only be expressed in the policy itself. For a complete explanation of coverages, please consult one of our licensed agents.

-

National Preparedness MonthSeptember 09, 2021

September is National Preparedness Month! Having a plan for when disaster strikes at home, at work or on the go can make a huge difference in the impact an event will have on you and your family. Visit http://www.ready.gov/september to see the recommended plans for the month.In the spirit of preparedness, don’t forget to read your insurance policy and check with your insurance agent to be sure you are protected against disasters that might happen in your area. Take some time to inventory your belongings in case the unthinkable happens. The National Association of Insurance Commissioners (NAIC) has developed a downloadable PDF to help you catalog those. Creating a home inventory will also help you determine if you have enough coverage for your belongings. Consult your licensed insurance agent for assistance in understanding or altering your coverages.

The biggest hurdle to overcome in being prepared is planning. While we all hope we won’t need to use our plans, disaster can strike anywhere at any time.

This information is meant to be a broad overview and should not be the only source you consult for evaluating your risk management needs. Adherence to the above guidelines does not ensure coverage under your policy, nor does it guarantee your risk will be accepted by our company or that your property or operations are safe, healthful, or in compliance with laws, rules, or regulations. Coverage is determined by specific policy provisions, limitations and exclusions that can only be expressed in the policy itself.

-

Your Cyber Security MattersAugust 18, 2021

Every day, we place our private data in the hands of other companies and individuals and trust them to keep it safe. Every day, bad actors are trying to steal that data. Unfortunately, some of them succeed.T-Mobile recently announced a data breach affecting 7.8 million customers. They estimate an additional 40 million records were stolen from past or prospective customers.

While no one can guarantee you protection from such a breach, you can take steps to insulate yourself from the aftermath of a stolen identity or other cybercrimes. Barton Mutual has partnered with Berkley Re to offer cyber liability coverage on many of our policies.

For our commercial policies, the coverage is optional and will offer assistance with a breach:

- First-Party Privacy Breach Expense, including up to $10,000 each for Extortion Threat Expenses, and Data Replacement and System Restoration Expense

- Third-Party Cyber Liability Coverage, including up to $10,000 for PCI Fines

- Regulatory Proceeding Claim Expense, including up to $10,000 for Regulatory Fines

- Optional First-Party Business Interruption, which equals 25% of the aggregate limit.

The Standard Aggregate inclusive of all coverages above is $25,000, with optional limits available of $50,000, $100,000 and $250,000. These coverages include additional services, such as:

- Notification letter preparation, printing and mailing

- Toll free number to Sontiq’s Resolution Center

- Call handling

- Credit monitoring and fraud alerts

- Fraud resolution services

- Investigative and forensic services

For most owner-occupied personal lines policies, the coverage is included and provides the following benefits:

- Online Extortion. Expenses and ransom paid for threats to cause a network disruption.

- Cyber Bullying Response. Costs for counseling, tutoring, temporary relocation, tuition expense.

- Identity Theft. Costs and help in reclaiming your policyholder’s identity.

- System Compromise. Data recovery and system restoration needs.

- Internet Clean Up. Expenses associated with removing false statements on the internet.

- Breach Cost. Costs associated with notification, investigation and monitoring a breach.

- Social Engineering. Costs that arise from the intentional misleading of an individual which leads to the insured willingly sending money to a fraudster.

Services for personal lines coverage include:

Identity Management

- Provides unlimited 24/7 service and support to help minimize damage and resolve identity theft incidents.

Ransomware

- Diagnose the issue and implement a plan to protect data.

- Get access to highly experienced professionals with deep expertise in information security, data privacy and governance.

- Receive customized ransomware risk assessment and prevention services.

Breach Protection

- Investigation of a breach and corresponding legal requirements.

- Notification services to alert anyone affected by a breach.

- Monitoring provided for those affected by a breach.

Educational Services

- Partnership with Nobully.org, a nonprofit working to eradicate cyberbullying worldwide.

- Alerts on the latest scams, fraud attempts and ways to prepare.

- Alerts on the latest malware and how to stay safe online.

Sontiq Claims

- Personalized handling of any cyber liability claim.

This information is meant to be a broad overview and should not be the only source you consult for evaluating your risk management needs. Adherence to the above guidelines does not ensure coverage under your policy, nor does it guarantee your risk will be accepted by our company or that your property or operations are safe, healthful, or in compliance with laws, rules, or regulations. Coverage is determined by specific policy provisions, limitations and exclusions that can only be expressed in the policy itself.

-

National Insurance Awareness Day 2021June 28, 2021

Monday, June 28 has been designated National Insurance Awareness Day. Your agent is ready to assist you in reviewing your insurance coverage and any potential needs for coverage. You should consider carrying insurance for property you own, property you rent to or from others, and liability for your personal protection. A call to your agent can assist in determining if you have adequate coverage. Be sure to mention what has changed since any of your existing policies were issued.

Some changes are significant and can affect your coverage, so be sure and discuss any changes you have made. Adding or removing wood heat, other adults living in the home, renovations and purchases are examples of things you should discuss. Please don’t wait for a claim to happen before you contact your agent!

Also consider an annual update to your personal inventory to be sure you have a current list of all your belongings. If you don’t already have a list, you can download a PDF file or order a hard copy booklet for tracking your home inventory from the Missouri Department of Insurance: https://insurance.mo.gov/consumers/home/homeinventorychecklist.php.

We would love the opportunity to serve you by providing for your insurance needs. Find an independent agency in your area that represents our company: https://bartonmutualgroup.com/agents.

This information is meant to be a broad overview and should not be the only source you consult for evaluating your risk management needs. Adherence to the above guidelines does not ensure coverage under your policy, nor does it guarantee your risk will be accepted by an insurance company or that your property or operations are safe, healthful, or in compliance with laws, rules, or regulations. Coverage is determined by specific policy provisions, limitations and exclusions that can only be expressed in the policy itself.

-

Tips to Prevent Loss While Working From HomeMay 12, 2021

More people than ever are working at home and taking classes from home, and they are doing it with more people in the home. This can lead to additional loads on electrical systems and devices. In a recent issue of the Mutual Boiler Re Gears in Motion, they addressed ways you can help prevent loss while working from home. For tips on maintaining the life of your technology devices or appliances, read their article: https://www.mbreonline.com/mbre/gim.nsf/May2021/currentarticles/losspreventionspring21/index.html.We partner with Mutual Boiler Re to provide Equipment Breakdown coverage on most of our policies for only $25 annually. If you are interested in learning more about this coverage or adding it to your policy with us, contact your agent today! If you want to find an agent in your area who represents Barton, search for your zip code on our agent finder: https://bartonmutualgroup.com/agents.

-

Time for an Annual Credit Check?April 26, 2021

As a consumer, you have a right to view your credit report from each of the three credit reporting agencies (Experian, TransUnion and Equifax) each year. Visit annualcreditreport.com to request the free report. You will have to pay to receive your credit score. It is important to review your report to verify that the credit information reported is accurate. Your credit report can affect your ability to finance items like houses and cars, and it can even affect your potential employment or your insurance rates. For more information on requesting the report, along with instructions for what you can do if you find errors, visit the Federal Trade Commission website.If you have minor children, you can ask the credit bureaus if a credit report exists for them. The Consumer Financial Protection Bureau (CFPB) has an article with tips on how to do that. You can request the file from any of the three bureaus. This is especially important if you believe your child may have been the victim of identity theft. If you discover that your child has a credit file, you can dispute the error. This tip sheet from the CFPB includes information on how to dispute the credit file for your child.

This information is meant to be a broad overview and should not be the only source you consult for evaluating your risk management needs. Adherence to the above guidelines does not ensure coverage under your policy, nor does it guarantee your risk will be accepted by our company or that your property or operations are safe, healthful, or in compliance with laws, rules, or regulations. Coverage is determined by specific policy provisions, limitations and exclusions that can only be expressed in the policy itself.

-

Protect Tax Returns and Stimulus Payments from Identity ThievesMarch 05, 2021

Over the past several years, the IRS actions against tax identity fraud were successful in driving down the rate of tax fraud. Then the COVID-19 pandemic happened. The IRS extended due dates and become bogged down trying to process returns while keeping their employees safe. Additionally, U.S. stimulus payments were administered as tax refunds and the Federal government enhanced state unemployment benefits. Identity thieves had more financial incentive than ever before to commit tax and benefits fraud.The impact was immediate: By the end of February 2020, tax return identity theft was already up 751% year over year.1 By June, 892,777 tax returns had been flagged by the IRS for potential identity theft.2 But there’s good news—you can take steps now to protect your identity as well as any tax refunds or stimulus payments due to you in 2021.

How tax return fraud happens

Tax-related identity theft can leave taxpayers bewildered and frustrated, but the mechanics of it are fairly simple. First, identity thieves obtain sensitive information about you including your name, address, and personal tax identification number. They can either buy the information from criminal sources or trick you into giving it to them through phishing or phone scams. Then they use it to file a tax return using a false address or post office box and wait for the refund check to roll in.

Warning signs of tax return fraud

There are several warning signs that indicate you may be a victim of tax return fraud:

- The IRS or other taxing authority rejects your attempt to file your tax return.

- The taxing authority requests verification of your identity, indicating something may be amiss.

- Income is reported by two or more employers, most likely because someone else has used your tax identification number to gain employment. Your return could be flagged for failing to pay sufficient taxes on wages or to report all wages.3

Take advantage of the new IRS Identity Protection PIN

In January, the IRS expanded the Identity Protection PIN Opt-In Program to all taxpayers who can verify their identities.4 The Identity Protection PIN (IP PIN) is a six-digit code you establish with the IRS that is only known by the agency and you. The IP PIN provides a good way to lock out identity thieves and prevent them from filing fraudulent tax returns using your personal information. The IP PIN is valid for one calendar year, so mark your calendar to obtain a new one at the start of each year.

Resolve tax-related identity theft

If you discover you have become a victim, follow these steps:

- Contact your taxing authority and fill out identity theft paperwork.

- File your correct return using the instructions they provide you.

- Contact the credit bureaus and place a fraud alert on your account.

- Respond promptly to all correspondence from your taxing authority.

- Keep excellent records of all of your correspondence and filings.

- Add a credit monitoring and identity protection service to identify any further identity theft or fraud in other areas of your life.

We have partnered with CyberScout to offer comprehensive identity management services. Contact a local independent agent today to see how you can get a policy containing cyber protection with Barton Mutual.

1 “Interim Results of the 2020 Filing Season,” Treasury Inspector General for Tax Administration, April 7, 2020.

2 “Interim Results of the 2020 Filing Season: Effect of COVID-19 Shutdown on Tax Processing and Customer Service Operations and Assessment of Efforts to Implement Legislative Provisions,” Treasury Inspector General for Tax Administration, June 30, 2020.

3 “Taxpayer Guide to Identity Theft,” IRS website, page updated October 22, 2019.

4 “All taxpayers now eligible for Identity Protection PINs,” IRS, January 12, 2021.

-

Equipment Breakdown CoverageMarch 01, 2021

Our Equipment Breakdown coverage broadens your policy and covers against loss by mechanical or electrical breakdown that is otherwise excluded. This coverage is only available on certain policy types. See your agent or call our Customer Service department at x451 for details.

This coverage can protect you against loss of your electrical or mechanical equipment due to breakdown or failure. Now you can have protection for situations such as:

- Your air conditioning unit experiencing a mechanical breakdown mid-heat wave

- Your commercial refrigerator having a power surge on a hot day

- Your computer system having an electrical breakdown

Included with this coverage is our green equipment breakdown endorsement, which gives you incentive to repair or replace damaged property in an environmentally friendly way. When you experience a loss of mechanical, electrical or pressure equipment, you’ll have the opportunity to go green.

This information is meant to be a broad overview and should not be the only source you consult for evaluating insurance coverage or purchase. The description of coverages and programs are purposely brief and are subject to specific policy provisions, limitations and exclusions that can only be expressed in the policy itself. For a complete explanation of coverages, please consult one of our licensed agents.

-

Travel in Winter WeatherFebruary 08, 2021

Winter weather is here! While the safest bet during winter weather is to stay off the roads, some travel may be necessary. If you have to be on the road in such conditions, there are some things you can do to prepare for potential hazards:

- Allow for extra travel time.

- Travel at a safe speed, and leave plenty of room between you and other cars.

- Clear all surfaces of your car before you embark on your journey.

- Be sure your cell phone is fully charged. Bring a charger along if you have one that works in the car.

- Tell someone where you are going and how long you expect it to take you.

- Make sure you have a full tank of gas in case you do become stranded.

- Do not leave your vehicle if you become stranded. Tie a bright colored cloth to your antenna or door handle and attempt to contact emergency personnel via cell phone if you have one.

- If stranded, drivers should start and run their car for 10 minutes every hour, using the heater. Be sure that your exhaust pipe and radiator are clear of packed snow before running your engine. While the engine is running, partially open a down-wind window to avoid carbon monoxide poisoning and to get fresh air into the vehicle. Keep the vehicle’s interior lights on while the engine is running. Avoid hypothermia by constantly moving your arms and legs; clapping hands will help keep you warm as well. Warning signs of hypothermia are memory loss, disorientation, incoherence, slurred speech, drowsiness, exhaustion and uncontrollable shivering.

This information is meant to be a broad overview and should not be the only source you consult for evaluating your risk management needs. Adherence to the above guidelines does not ensure coverage under your policy, nor does it guarantee your risk will be accepted by our company or that your property or operations are safe, healthful, or in compliance with laws, rules, or regulations. Coverage is determined by specific policy provisions, limitations and exclusions that can only be expressed in the policy itself.

-

Protect Your Business During Winter WeatherJanuary 25, 2021

Our partners at Mutual Boiler Re developed a helpful infographic for businesses to suggest preventative maintenance to combat winter weather: protect your pipes, maintain the heat, prepare for power outages, and prepare your building for ice and snow. View the entire infographic for more detail and additional tips.

You should review your insurance policy with your agent to be sure your business is covered in the event of a winter weather loss. Barton Mutual offers Equipment Breakdown coverage on our commercial policies (in partnership with Mutual Boiler Re), which could be an enhancement of the coverage your policy already provides.

This information is meant to be a broad overview and should not be the only source you consult for evaluating insurance coverage or purchase. The description of coverages and programs are purposely brief and are subject to specific policy provisions, limitations and exclusions that can only be expressed in the policy itself. For a complete explanation of coverages, please consult one of our licensed agents.

-

January Maintenance and Organizing IdeasJanuary 11, 2021

In January, you probably spend time recovering from the holiday madness and huddling at home waiting on spring. If you want to get a head start on some home maintenance and organizing, check out these suggestions from Realtor.com (view the full article for additional tips: https://www.realtor.com/advice/home-improvement/monthly-home-maintenance-checklist-january/):- Recycle your holiday cards into gift tags for next year.

- Deep clean areas of your home that don’t always get attention: range hoods, refrigerator coils, ceiling fans, light fixtures, door knobs, etc.

- Declutter! Find things you can donate, sell or dispose of.

- Begin planning for your garden.

Winter in Missouri is usually more pleasant inside, and all of those items can be done from the warmth of your home. Save the outdoor maintenance for nicer days ahead!

This information is meant to be a broad overview and should not be the only source you consult for evaluating your risk management needs. Adherence to the above guidelines does not ensure coverage under your policy, nor does it guarantee your risk will be accepted by our company or that your property or operations are safe, healthful, or in compliance with laws, rules, or regulations. Coverage is determined by specific policy provisions, limitations and exclusions that can only be expressed in the policy itself.

-

The Retirement AdventureDecember 30, 2020

Two of our amazing employees have determined that December 31 is the end of their career journey and the beginning of the new adventure in retirement.

Linda McKay began as a billing clerk at Barton in 1975. She worked her way up to Personal Lines Underwriter, where she remained for many years, eventually becoming Personal Lines Manager. She stepped up to fill the Director of Policy Production role for us in 2012, and she stayed there until the beginning of this year. She transitioned back to personal lines underwriting, where her passion lies. She worked in underwriting this year, spending the second half of the year training with new hires. We appreciate the service Linda has given to Barton all these years, and we wish her the best in her retirement. We’re sure to see her frequently, as she and her sister run a bakery across the street from our office. Hopefully her husband, two children and two grandchildren also benefit from her additional “free time.”

Larry Bahr joined the Barton family in 2009 as a Personal Lines Underwriter. He came to us with several years of experience. We’ve grown to deeply appreciate Larry, especially when we have—er—plumbing issues. His title of Chief Toilet Officer (CTO) was not bestowed lightly. Even though we will miss Larry, we know he is going to enjoy his new adventure, and we still have his number saved in case we ever spot a snake anywhere near the office. We are hopeful that his new status of “retired” will afford him more time to do the things he loves and spend more time with his three children.

-

Home Safety Tips for the Holiday SeasonDecember 11, 2020

We have compiled a few friendly reminders on how you can take steps to help protect your home from burglars and other potential harm this holiday season. Portions of this were taken from an article on www.safewise.com.- If you can afford a home security system or security cameras of any kind, those are both great ways to protect your home. If you can’t afford those, you can try putting a security sign in your yard or setting up a dummy camera to convince would-be burglars that you do have one.

- Don’t advertise your travel plans on social media. That just gives burglars a precise schedule to find your home unoccupied. Post those pics after you return home.

- Install motion sensors on any outdoor lights you have. Use a timer on Christmas lights to make sure they come on as scheduled while you are gone.

- Consider leaving on a radio or TV during the day that could convince a burglar that someone is in the home.

- This seems pretty obvious, but lock your doors and windows. This includes keeping your garage door closed as much as possible. An open garage door may seem like an invitation, and it shows off your stuff to passersby.

- If you are going to be away for more than a couple of days, have the Post Office hold your mail and stop any newspaper deliveries. You could also ask a friend or trusted neighbor to pick up your mail and papers. Nothing signals an absence like a pile of newspapers in the driveway.

- Be friendly to your neighbors. Having a good relationship with those who live around you can supply an additional layer of security for your home. They can keep an eye out when you are gone, and you can return the favor when they leave home.

- Reduce the landscaping around your home. This may seem like an odd addition to the list, but bushes and shrubs around a home make good hiding spots.

- At Christmastime, keep packages out of view of the windows. Passersby shouldn’t be able to tell how many packages little Suzie has under the tree.

- Consider contacting your local police department to do a check of your house. They might be able to suggest things you could do to improve security.

This information is meant to be a broad overview and should not be the only source you consult for evaluating your risk management needs. Adherence to the above guidelines does not ensure coverage under your policy, nor does it guarantee your risk will be accepted by our company or that your property or operations are safe, healthful, or in compliance with laws, rules, or regulations. Coverage is determined by specific policy provisions, limitations and exclusions that can only be expressed in the policy itself.

-

Up on the Rooftop…November 12, 2020

In two short weeks, we will celebrate Thanksgiving. Your mind may already be drifting toward Christmastime, or you may have started the decorating process. Hanging outdoor lights is a popular tradition, and many people enjoy taking their decorating game to the next level, and still more like seeing elaborately decorated homes and businesses. Whether you are an avid, experienced light-hanger or a first-timer, there are lots of things to consider and some safety to keep in mind. This post from Lowe’s offers some basic tips for anyone wishing to light up their home this Christmas. Make sure you have the right tools and be safe out there displaying your holiday spirit!This information is meant to be a broad overview and should not be the only source you consult for evaluating your risk management needs. Adherence to the above guidelines does not ensure coverage under your policy, nor does it guarantee your risk will be accepted by our company or that your property or operations are safe, healthful, or in compliance with laws, rules, or regulations. Coverage is determined by specific policy provisions, limitations and exclusions that can only be expressed in the policy itself.

-

Here Comes Winter!October 26, 2020

Today, we are getting a cruel reminder that winter is just around the corner. As temperatures drop in the coming weeks, make sure your property is prepared and your insurance policy is equipped to provide coverage in the event of a winter weather loss.

- Always maintain heat during winter months, even in vacant dwellings/businesses. If you are going to be away from your home, you can reduce the heat so it won’t run as much, but ensure it’s not too low, as water lines in exterior walls could freeze in times of extreme wind chill or temperature drops.

- Winterize your pipes when possible and, again, maintain heat at an appropriate level; simply leaving it above freezing will most likely not be sufficient. Freezing pipes and the resulting damage may not be a covered loss under certain types of insurance policies. In addition, policies that do contain coverage for the peril of freezing may not cover loss that results from your failure to maintain heat or properly winterize the structure.

- Turn off the water and winterize the lines at your home if you’re leaving for a few days. This can mitigate the possibility of a water-related loss while you are away.

Check with your insurance company or agent if you need help understanding your policy, and brace yourself for winter!

This information is meant to be a broad overview and should not be the only source you consult for evaluating insurance coverage or purchase. The description of coverages and programs are purposely brief and are subject to specific policy provisions, limitations and exclusions that can only be expressed in the policy itself. For a complete explanation of coverages, please consult one of our licensed agents.

-

Safe Online Shopping Guidance for the Holidays and Cyber WeekOctober 20, 2020

Smartphones and the Internet have revolutionized the way consumers shop. Armed with a few search terms and simple clicks, we can find items, compare prices, read product reviews, order, and pay for all types of items from electronics, appliances, and tools to furniture, clothes, and groceries. Often, consumers also have the power to choose whether purchases will be picked up in store or delivered right to our doorstep. Any way you look at it, online shopping is a fast and convenient way to buy what we want and need.Online convenience also comes with some risk. Sometimes consumers don’t receive exactly what they ordered; get scammed by fraudulent websites; or become victims of identity theft and/or loss. Cybercriminals are opportunistic, and they will be seeking to exploit the growth in online shopping this holiday season. But don’t worry, with a little preparation and vigilance, consumers can safely and securely shop online and avoid falling victim to scams.

Since cybercrime is largely motivated by money, that makes Black Friday and Cyber Monday very attractive targets for cybercriminals. And that means increased phishing attempts that try to get you to reveal personal information, account credentials, and credit card numbers. Through email, fake ads, and illegitimate websites, cybercriminals are hoping some unwitting consumers will let their guard down in the rush to secure the best deals before they’re gone.

Since consumers often spend more than usual during the holiday season, it’s easy to lose focus when an email or text message arrives under the guise of your credit card provider or bank regarding a suspicious transaction or frozen account. Without prior awareness of these scams, some consumers mistakenly click on links or share their personal information. Instead, consumers should be aware of these and other common attacks and use caution to avoid falling victim.

Knowledge is power. Enjoy your online shopping experience by following best practices and increase your awareness of common scams. These eight tips can help you get the deals and avoid the scams:

- Use familiar websites and know thy vendors. Before providing any personal or financial information, be sure that you are doing business with a reputable, established vendor. Verify the legitimacy of the website by reviewing certificate information, including who it was issued to. Check the BBB’s online directory and scam tracker or search retailer reviews on Google.

- Look for the ‘s’ and the lock. Always look for the security symbol, such as an unbroken padlock in the address bar and URLs that start with ‘https’. This ensures that your information is protected with encryption.

- Avoid phishing and social engineering attacks. Be wary of unsolicited email requesting information from you, such as fake invoices or shipping notifications. Legitimate businesses don’t ask for information via email. Instead of responding to the email or clicking on links, type in the merchant’s authentic website address yourself and log in to check your account.

- Be aware of common tricks. Educate yourself about common online scams to avoid falling for too-good-to-be-true deals, including rock-bottom prices form unknown internet retailers, fake ads and social media offers, gift card scams, and more.

- Use credit, not debit. Credit cards offer an extra level of protection from fraudulent charges that may not be available with a debit card. You can add additional purchase protections by using a payment gateway like PayPal, Good Wallet, or Apple Pay. Secure payment gateways stop purchase data from being intercepted by hackers.

- Monitor your statements and verify receipts. Keep records of your purchases, including confirmation pages or email receipts, to compare with your bills and statements. If there is a discrepancy, report it immediately.

- Always use strong passwords. Simple and commonly used passwords allow hackers to easily gain access and control of your online accounts, change shipping addresses, and make purchases using your credit cards.

- Don’t purchase over public Wi-Fi. If you shop using your mobile phone, stay on your carrier’s cellular network. Free public Wi-Fi can be much less secure.

CyberScout®—We’ll take it from here.™

CyberScout is leading the charge against hackers and thieves, providing identity management, credit monitoring and cyber security for more than 17.5 million households and 770,000 businesses. Contact your bank, credit union, insurance company or employer to find out if they offer CyberScout services.

This information is meant to be a broad overview and should not be the only source you consult for evaluating your risk management needs. Adherence to the above guidelines does not ensure coverage under your policy, nor does it guarantee your risk will be accepted by our company or that your property or operations are safe, healthful, or in compliance with laws, rules, or regulations. Coverage is determined by specific policy provisions, limitations and exclusions that can only be expressed in the policy itself.

-

October: National Financial Planning Month & National Cyber Security Awareness MonthOctober 05, 2020

Adequate insurance coverage is an important part of any financial plan. Some common areas that may be overlooked include home-based business coverage, equipment breakdown coverage, insured values on property (especially if improvements have been made), and ACV vs. replacement cost coverage. It might also be a good idea to review the deductible on your policies to be sure you are financially capable of assuming that cost in case of a covered loss. Your insurance agent can help you understand your coverages and determine if you are adequately covered in case of a loss.October also happens to be National Cyber Security Awareness Month. At Barton, we offer cyber liability coverage for the majority of our owner-occupied policies and as an option for our commercial policyholders. One of our partners in this endeavor is CyberScout. They offer an online tool called ID RiskCompass that can help you evaluate your risk of ID theft and help you think of ways you can better protect your identity. You can also visit their Knowledge Center to find tips on protecting all elements of your identity.